Wendi by Waave: Open Banking Acquisition Engine

Owned end-to-end: Problem discovery → Banked acquisition (2024). Cut consent friction 50%+ → PLG scale → payments revenue.

Infrastructure ready. Consumers blocked by trust.

Open Banking in Australia was built on the promise of consumer control, transparency, and secure data sharing through the Consumer Data Right (CDR). In practice, that model introduced a behavioural challenge: users still had to overcome fear, effort, and uncertainty before connecting their bank accounts to a third-party service.

Consumer adoption was much lower than infrastructure readiness suggested. A 2024 strategic review noted that at the end of 2023, only 0.31% of bank customers had an active data-sharing arrangement — while industry commentary called for simpler consent experiences and clearer consumer propositions.

of bank customers with active data-sharing (end of 2023)

The trust gap between what Open Banking could do and what consumers were willing to try was the single biggest obstacle to growth.

Competitive Landscape (2023)

Australia's automated subscription-tracking space was sparse. Most alternatives were manual-entry tools, full budgeting apps with secondary features, or global apps lacking local bank support — highlighting Waave's first-mover edge via CDR/Open Banking.

| Competitor | Automation | Open Banking | Pricing | Key Limitation |

|---|---|---|---|---|

| Wendi | Full (bank sync) | ✓ CDR | Free | N/A — purpose-built |

| Frollo | Transaction cat. | ✓ CDR | Free | No dedicated subs dashboard |

| PocketSmith | Transaction cat. | ✓ Basiq | $10+/mo | No sub-specific tools |

| TrackMySubs | None | ✗ | Free–$5/mo | Manual entry only |

| SubTracker | Statement AI | ✗ | $13 one-time | No real-time sync |

| Rocket Money | Full | ✗ (US only) | $4–12/mo | No AU bank support |

Ideal Customer Profile

ICP: 25–45yo urban pros wasting $670/yr on subs. Wendi = first-mover sub hunter.

Demographics

- →Australians aged 25–45, urban (Sydney/Melbourne)

- →Middle-income professionals/families ($60k–$120k)

- →Tech-comfortable, responsive to savings hooks

Pain Points

- →Overlooked subs — avg. AU household wastes $670/yr (NAB)

- →Bank juggling across multiple accounts

- →Cost-of-living squeeze driving savings urgency

Behaviours

- →70% aware of subs but only 40% actively track them

- →Use budgeting apps, open to new fintech tools

- →Share savings tips socially — viral potential

Why Wendi Fits

Frictionless CDR flow delivers value in <2 minutes, building trust that leads to the payments upsell. Free, instant, and sub-focused — exactly what the ICP needs, exactly when cost-of-living pressure peaks.

Value exchange > data rights talk

Waave recognised that trust in Open Banking would not be won through abstract messaging about data rights alone. The business needed a value exchange strong enough to justify consent, especially in a market where consumers were already overloaded by subscription costs and sceptical of sharing financial data.

The product insight: subscription tracking is an easy-to-understand pain point with immediate personal value. If users could quickly discover forgotten or duplicated subscriptions, Waave could turn a high-friction data-sharing decision into a practical money-saving action.

Free sub tracker = consent gateway to Pay by Bank.

The shift

Mission-aligned from day one

Waave's mission is to leverage open banking data to reinvent payment experiences and create positive change for both businesses and consumers. Wendi wasn't a side project — it was the mission made tangible.

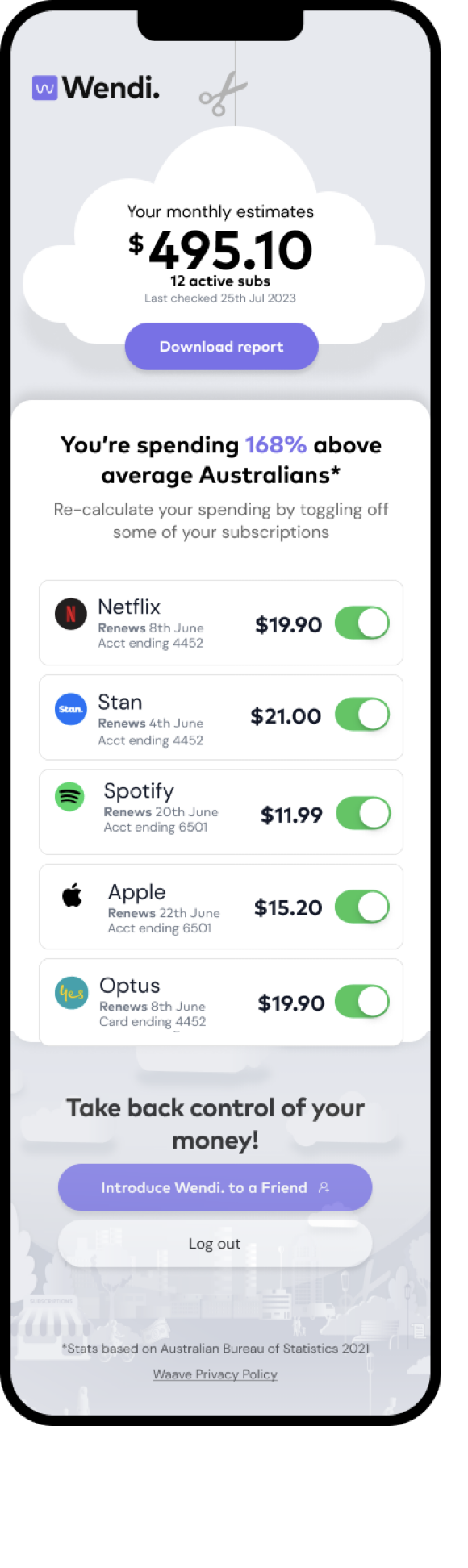

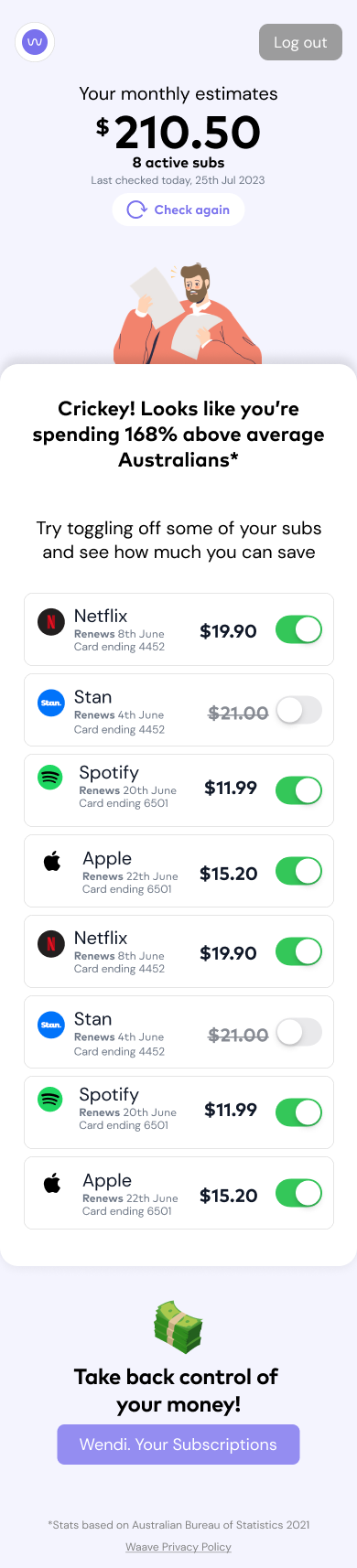

Save You Money

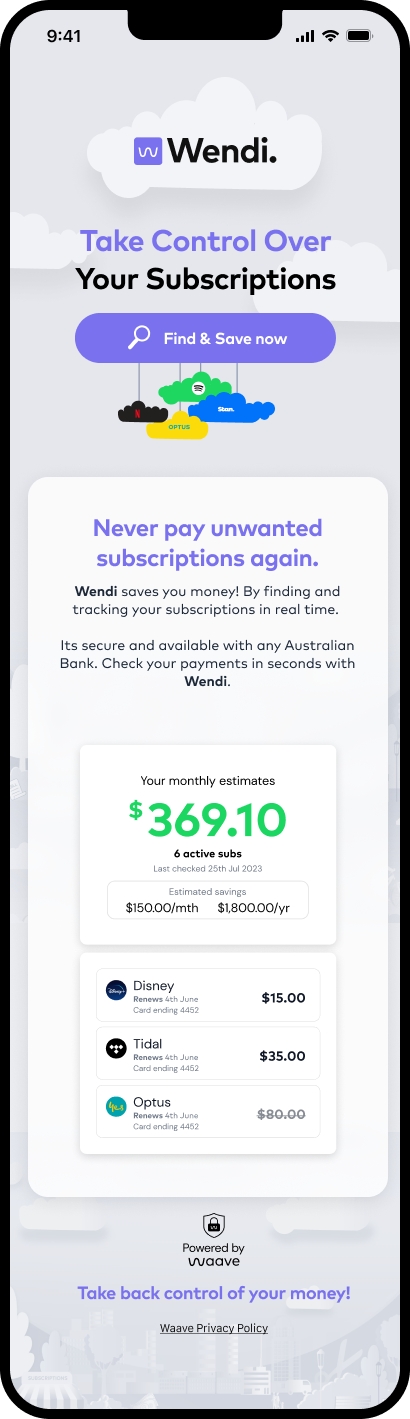

Identify duplicate and forgotten subscriptions. Wendi surfaces hidden costs so users save before Waave asks for anything.

Give You Back Control

Toggle services on/off, download spend reports. Control over data and spending — the CDR promise made real.

A Better Experience

Personalised insights powered by real transaction data. No generic advice — actionable, individual clarity.

Safer & More Secure

Bank-grade encryption. Read-only access. You own your data. Trust earned through transparency, not marketing.

7-Stage Product Design Framework

Applied JTBD + DSB standards: 3-step flow owns consent → dashboard. Cut consent friction 50%+ via regulatory-first design.

Discovery

User research, competitor audit, regulatory scan

Validated JTBD opportunity

Define

JTBD mapping, value prop, success metrics

Land-and-grow model defined

Ideate

Wireframes, trust cues, progressive disclosure

50%+ friction reduction designed

Design

Hi-fi mocks, compliance patterns, merchant mapping

DSB 5-stage compliance achieved

Validate

User testing, benchmarking, V1 product dev started

>80% activation target hit

Develop

Full V1: toggles, reports, brand icons, accreditation

Production-ready infrastructure

Launch

TV coverage, viral referrals, growth monitoring

PLG → acquisition

Discovery

Apr '23User research, competitor audit, regulatory scan

Validated JTBD opportunity

Define

May '23JTBD mapping, value prop, success metrics

Land-and-grow model defined

Ideate

Jun '23Wireframes, trust cues, progressive disclosure

50%+ friction reduction designed

Design

Jul '23Hi-fi mocks, compliance patterns, merchant mapping

DSB 5-stage compliance achieved

Validate

Aug '23User testing, benchmarking, V1 product dev started

>80% activation target hit

Develop

Aug–Sep '23Full V1: toggles, reports, brand icons, accreditation

Production-ready infrastructure

Launch

Sep '23TV coverage, viral referrals, growth monitoring

PLG → acquisition

Concept in March. Launched in September. 7 months, end-to-end.

End-to-End Product Leadership

The CDR consent process — and why most users quit

Australia's Consumer Data Right mandates a structured consent flow: Pre-Consent → Consent → Authenticate → Authorise → Post-Consent. While technically sound, this created a behavioural gauntlet that most consumers abandoned.

Industry research highlighted skepticism, ambiguity, and inertia around data sharing, with consumers feeling little control (average self-rating of 3 out of 7) and demanding clear value exchanges before consenting.

Waave leveraged deep regulatory knowledge of DSB standards and consultant insights — including progressive disclosure to avoid cognitive overload — to design a consent flow that minimised barriers while staying compliant.

of bank customers with active data-sharing (end of 2023)

Average consumer self-rating of data control

Standard CDR vs Waave's Wendi Flow

| Stage | DSB / CDR Standard | Waave / Wendi |

|---|---|---|

| Pre-Consent | Value prop and CDR education in data recipient space | "Take back control of your money!" + savings estimates upfront |

| Consent | Review who / what / when / where / why / how | Bank selection + simple user agreement; no lengthy T&Cs |

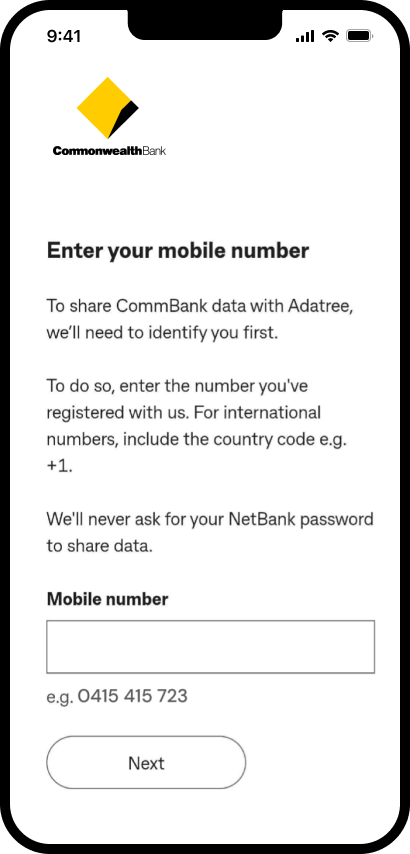

| Authenticate | Verify identity in data holder space | OTP mobile entry with reassurance ("never ask for password") |

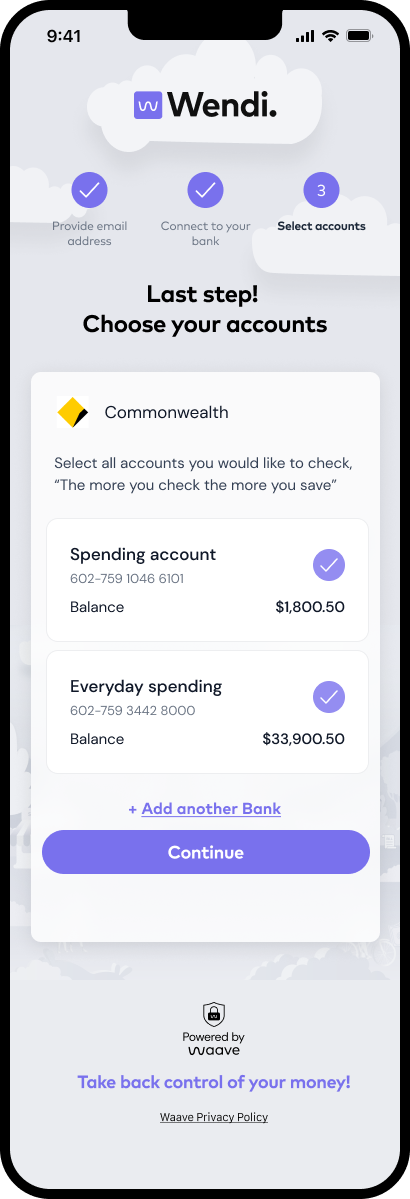

| Authorise | Select accounts, review data summary | Granular account choice ("Spending account 602-759") + balance preview |

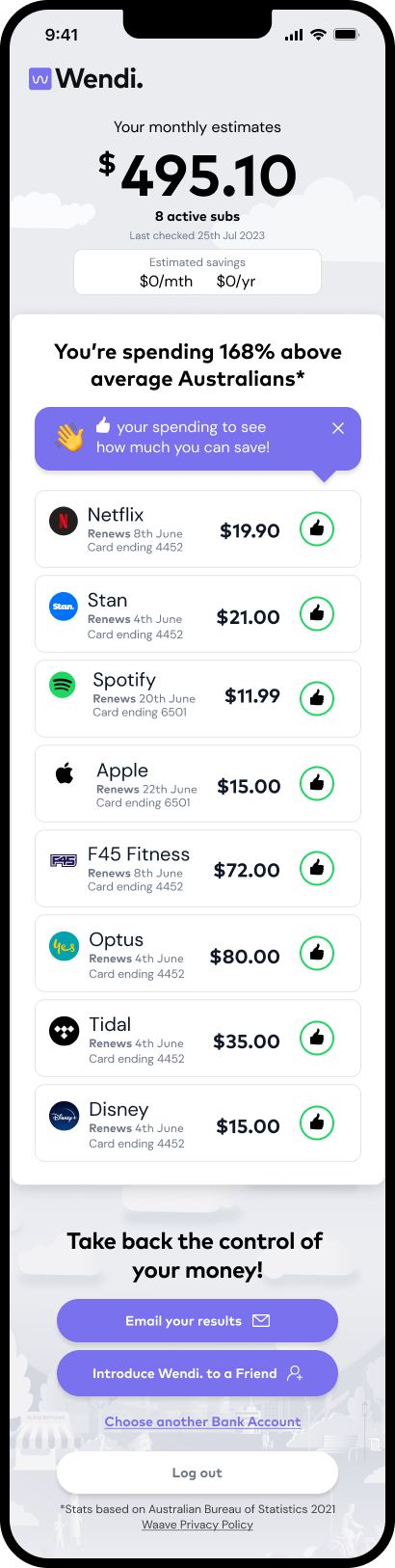

| Post-Consent | Share outcomes, close feedback loops | Immediate dashboard: subs listed, savings calculated, "Find/Save now" CTA |

Applied DSB standards and UX research to cut consent friction 50%+ — enabling viral consumer acquisition for payments monetisation.

— Portfolio insight

A 3-step flow that turned compliance into conversion

Waave's Wendi flow optimised the standard CDR model for subscription tracking, creating a seamless "value-first" experience. It started with a compelling pre-consent hook — "Never pay unwanted subscriptions again" — followed by minimal steps.

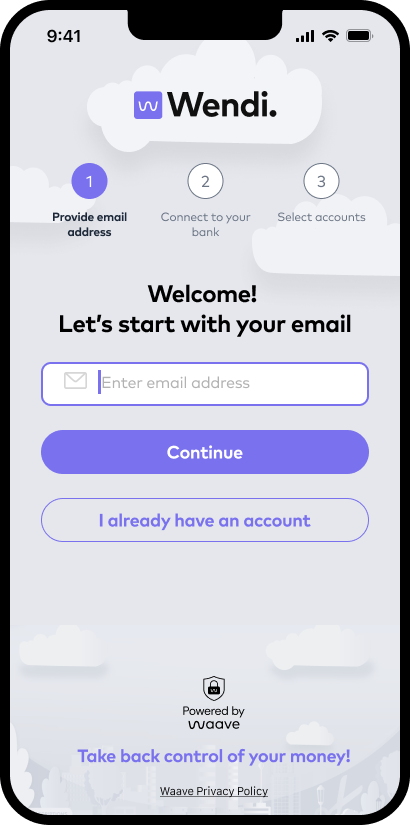

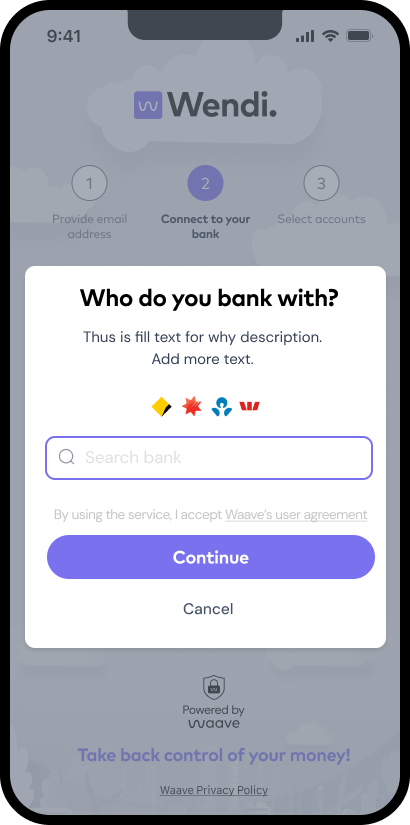

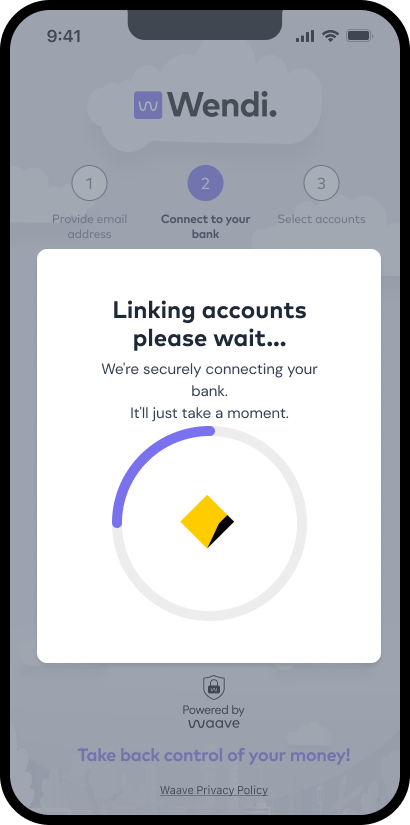

The typical CDR multi-screen burden was reduced to a 3-step core: Email → Bank → Accounts. Each screen used progressive disclosure — one decision per step — with explicit trust signals throughout.

Accredited via Adatree integration, Waave stayed fully compliant while humanising the experience — tying consent directly to a free, tangible benefit that users could see immediately.

Step 1: Email

Simple entry with 3-step progress indicator

Step 2: Bank Selection

Search your bank, accept user agreement — no lengthy T&Cs

Step 3: Account Selection

Granular account choice with balance preview

Trust reinforcement

"We'll never ask for your NetBank password to share data."

The complete Wendi user journey

Seven screens from landing to subscription insights — each designed to maintain momentum and reinforce trust at every step.

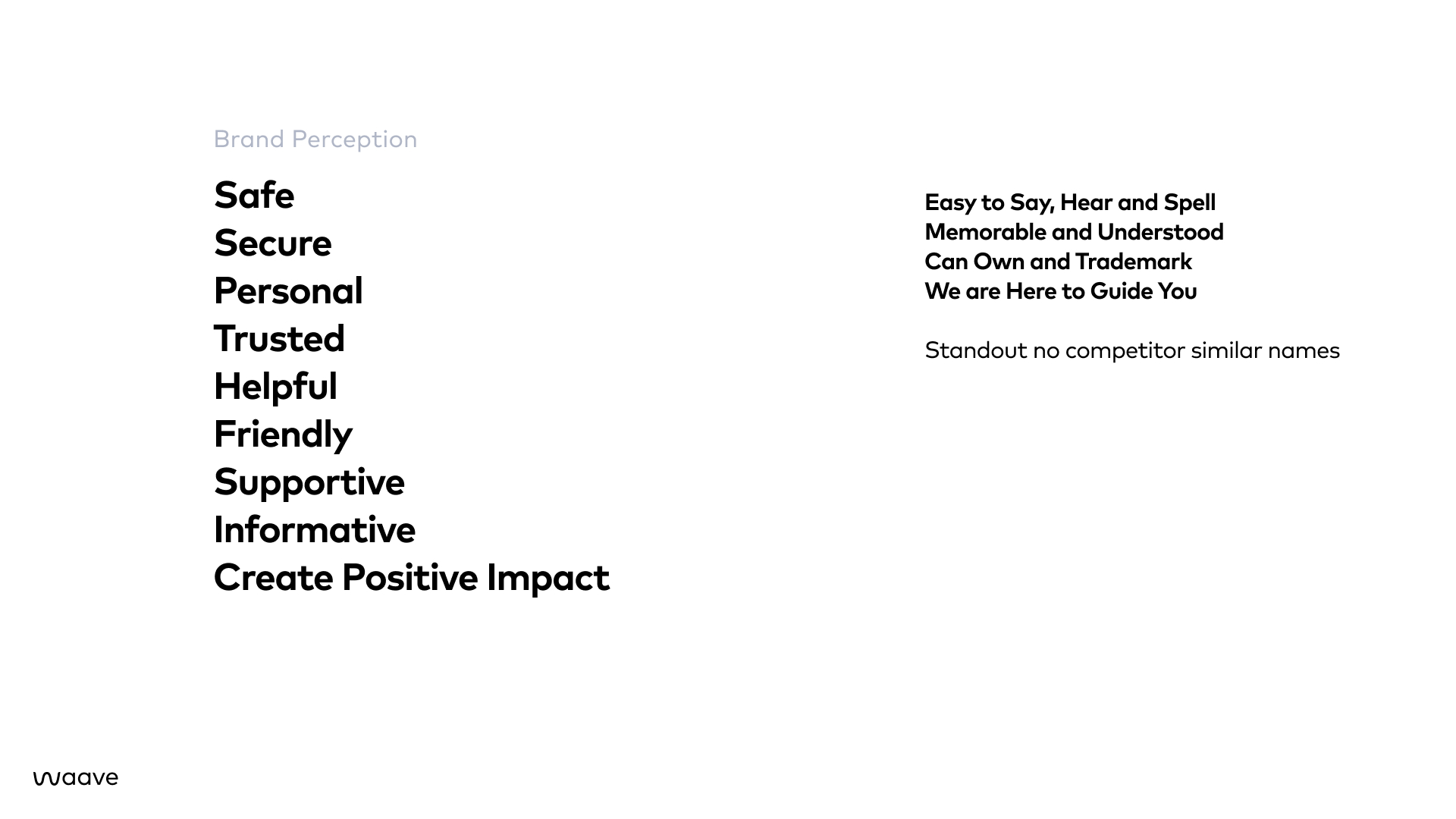

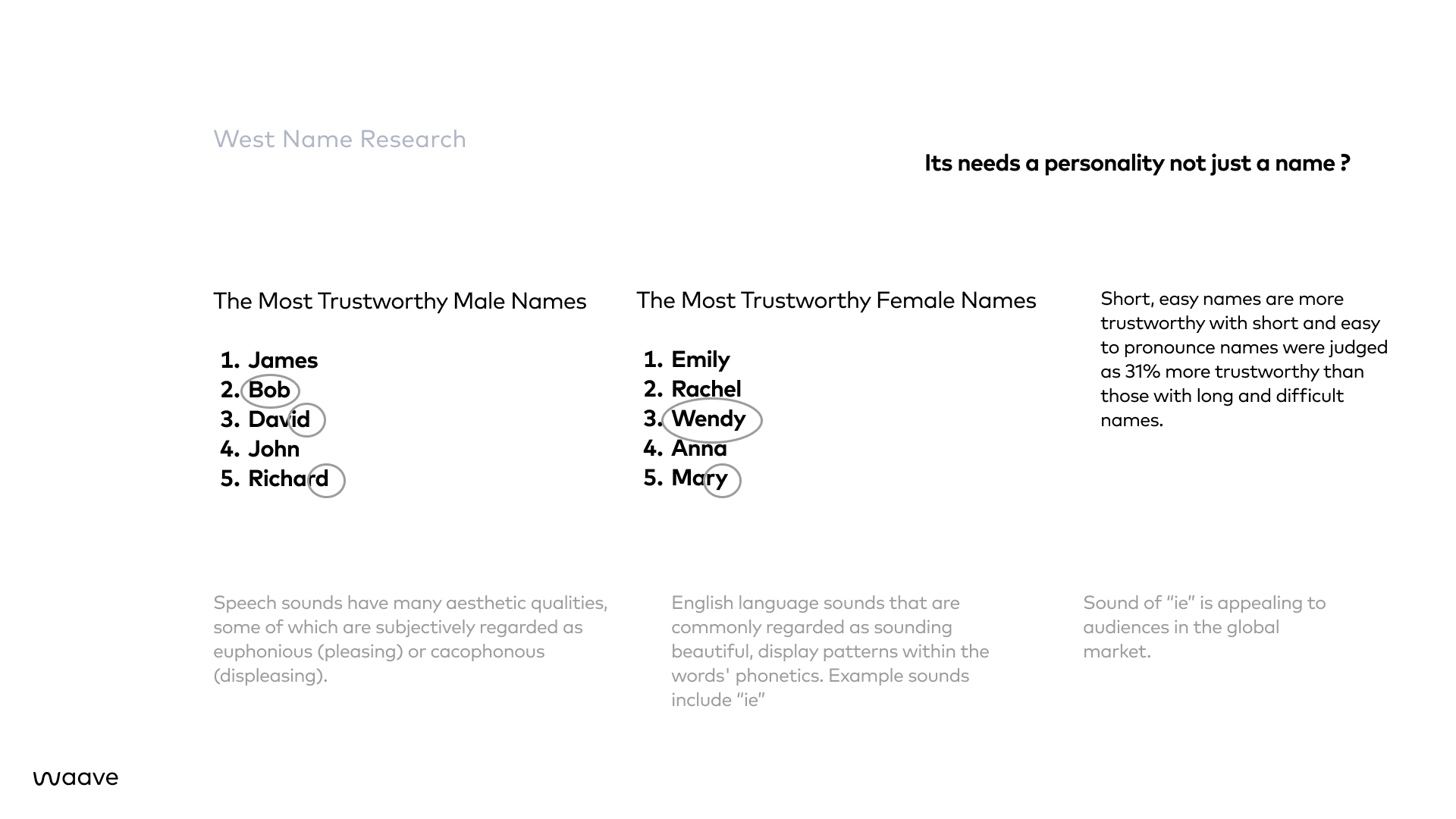

From "Health Check" to a name people trust

The original working name — "Health Check" — felt clinical, generic, and couldn't be trademarked. Consumers wanted a personality, not a product label.

Names ending in the "ee" sound tested highest for approachability across AU, UK and US markets. Wendi was born: warm, memorable, trademarkable, and ready for global markets.

Mobile-first design, desktop ready

Wendi was designed mobile-first with desktop availability — matching how consumers actually check their finances.

Design Principles

How do you present transactional data in a way consumers can consume and stay engaged? We needed it to load quickly, so the design elements were minimalistic with information presented in a well-formatted way.

Fast Loading

Minimalistic design elements — no bloat, just clarity. Web-first with no app download.

Well Formatted

Transactional data scrollable in date order. Clean hierarchy that's easy to scan.

Interactive Headline

Headline subscription number users could toggle to see the real impact of their spend.

Simple & Effective

Every screen designed for one action. Progressive disclosure kept cognitive load low.

Trust-Led Onboarding

The onboarding flow needed trust signals to overcome the data consent challenge. Time was invested in product messaging that led from the brand — giving Wendi a personality as an assistant who is helping you uncover any unknown subscriptions.

We used Look Who's Charging to provide accurate mapping of transactions to companies — displaying the correct merchant name and icon for visual recognition.

Concept in March. Launched in September. 7 months, end-to-end.

From platform data anatomy in March through Discovery, Define, Ideate, Design, Validate, and Develop — with parallel platform engineering running since June — Wendi shipped V1 in September 2023. Every screen had to earn its place under intense time pressure.

Design Evolution

Launch MVP

Core subscription insights with minimalistic UI — prove the value fast.

Trust Redesign

Refined messaging, improved visual hierarchy, stronger security signals.

Wallet — The Convergence

Wendi Insights and Pay by Bank converge into Wallet.

- → Unified balance

- → Toggle controls

- → Pay by Bank engine

57 beta testers. Real data. Clear signals.

We ran a structured feedback survey across Aug–Nov 2023 to validate the consent flow, subscription detection accuracy, and feature appetite before scaling.

80%

Rated connecting easy (1–2 / 7)

36%

Found forgotten subscriptions

73%

Liked the +/- calculator

61%

Would return weekly or monthly

Top Feature Requests

What users wanted next — ranked by frequency across 57 responses.

Usage Intent

How often users said they'd return.

61% indicated weekly or monthly return intent — strong retention signal.

User Voices

Direct quotes from beta testers.

"I just moved bank and used Wendi to check I moved all my subscriptions over. One came up which I'm sure I'd already moved."

"I felt the need to read through data policies… mostly due to a lack of trust in banks and what my bank may share."

"I love the concept of Wendi but it does not work for me for some reason."

"Potential to be a good tool if it works correctly."

Trust & Data Comfort

Users rated their comfort linking bank accounts at 4.4 out of 7 — reinforcing the CDR ecosystem's broader trust gap (only 0.31% national adoption by late 2023).

Low comfort (1–3)

37%

Cited distrust in banks sharing data

Moderate (4–5)

35%

Comfortable but read policies first

High comfort (6–7)

28%

Trusted the CDR consent flow fully

"I felt the need to read through data policies… mostly due to a lack of trust in banks and what my bank may share." — Beta tester

Consent Flow Connection: This mid-range trust score directly informed Wendi's "value-first" approach — showing savings estimates before asking for bank credentials, and reinforcing security messaging ("We'll never ask for your NetBank password") to bridge the comfort gap.

📊 Research Takeaway

The consent flow tested well (80% found it easy), but 39% reported missing subscriptions — highlighting the detection algorithm as the #1 area for improvement. The 4.4/7 trust score validated our consent UX strategy while revealing further opportunities to build confidence through transparency and value-first design.

Today Show launch → 10K+ users → Banked acquisition

Wendi's GTM combined a clear consumer hook with credibility through operating in the regulated Open Banking environment. AARRR: $0 CAC, viral referrals, payments path validated.

Growth Timeline

Mainstream credibility by design

Waave deliberately pursued mainstream media to build credibility beyond fintech audiences.

Channel 9 — Today Show

"Latest apps to help you spend smart and save big"

The segment drove a major spike in organic sign-ups, validating the strategy of using earned media for trust-building in a market wary of sharing financial data.

Watch on 9Now →Also featured in

Influencer Marketing

Targeted campaigns with finance-focused creators drove engagement and lowered CAC.

📋 PR Launch Strategy

Developed and executed a multi-phase PR strategy to drive user acquisition through earned media credibility — positioning Wendi as a consumer money-saving tool rather than a fintech product, solving the core Open Banking trust barrier.

Objectives

Primary

Drive users to Wendi

Supporting

- • Educate consumers on subscription money "traps"

- • Position Waave as advocate for fairness & transparency

- • Build awareness of Pay by Bank ecosystem

- • Create perception of brand momentum

Target Audiences

👤 Consumer

Primary

Gen Z & Millennials (18-42), Men, Couples with children

Secondary

Gen X (43-58), Women, DINKs

💼 Business / Investor

Tell the broader Waave growth story — Open Banking leadership, product ecosystem, and commercial traction to support investor confidence and consumer credibility.

Launch Tactics

🎯 Media Exclusive

Offered launch exclusively to a national outlet first. Targeted consumer TV (Channel 9 Effie Zahos, Sunrise) and business press (AFR, SMH).

📰 Dual Release

Consumer release (product + survey stats on subscription waste) and industry release (Waave ecosystem, Open Banking momentum) distributed nationally post-exclusive.

🤝 Case Study

Real consumer story for broadcast — "someone who knows they have too many subs but hasn't done anything about it" — making the abstract tangible.

Post-Launch & Growth PR

📊 Data-Driven Stories

- • Spending trend analysis from Wendi user data

- • "Cost of living" angles tied to interest rate rises

- • Average Australian subscription spend — end-of-year hooks

- • Annual "State of Subscription Spending" report

🌟 Influencer Strategy

Budget-permitting ambassador program — not confined to finfluencers. Targeted relatable, cross-platform personalities (e.g. Hamish & Andy, Zoe Foster Blake) who align with the fairness/savings brand.

Execution Timeline

Result

Today Show exclusive secured → 1,800 users in September → 10K+ by December

~$0 paid media spend. Earned coverage normalised bank-linking, lifted consent rates, and fuelled word-of-mouth referral growth.

September 2023

Australia's first instant-access, free subscription tracking tool

Wendi launched with a clear consumer proposition: connect your bank, see your subscriptions, find savings — free, in under 60 seconds. No app download required.

2024

Acquired by Banked

Banked specifically highlighted the work Waave and Chemist Warehouse were doing to create a low-cost, secure, engaging consumer experience for Pay by Bank — validating the land-and-expand thesis.

Waave's combination of Pay by Bank infrastructure and consumer-facing utility helped it establish enough traction to become an acquisition target — proving the commercial model worked.

5 keys: Trust-first, funnel inversion, risk removal, value unlock, PLG monetisation

This case demonstrates how product, GTM, and strategy can work together in a regulated market — and offers a playbook for product-led growth with enterprise monetisation underneath.

Trust is the true constraint

In regulated data markets, trust — not technology — is the bottleneck. Waave identified this early and designed everything around earning it.

Start with the hardest part of the funnel

Consent is where most Open Banking products lose users. By making consent the easiest step, Waave inverted the typical drop-off curve.

Remove consumer risk first

Free, no download, no ID verification, no commitment. Every potential objection was eliminated before the user could think of it.

Create obvious value before asking for anything

Wendi gave users something tangible — subscription visibility and potential savings — before Waave asked for any commercial engagement.

Let value unlock the commercial engine

Product-led growth with enterprise monetisation. The free tool created consented data access, which supported Pay by Bank revenue — a model elegant enough to attract acquisition.

Free land → consented data → Pay by Bank revenue → acquisition exit

The commercial logic was elegant: Wendi itself was free, but it increased the likelihood of consumer engagement with Waave's broader infrastructure — especially payment flows.

Waave's Pay by Bank proposition was built around lower merchant fees, instant authorisation, and a consumer experience that avoided card entry and reduced transaction risk.

Wendi was a strategic acquisition layer that supported future payments adoption. The company drew enough market relevance that Banked acquired Waave in 2024, citing its consumer experience and merchant relationships as part of the strategic rationale.

Pay by Bank advantages

- →Lower merchant fees vs card networks

- →Instant authorisation, no card entry

- →Reduced transaction risk and chargebacks

- →Consumer experience designed for trust

Validation

Acquired by Banked, 2024

Citing consumer experience + Chemist Warehouse partnership

🌱 Land

- ✓Free consumer insights tool — zero friction sign-up

- ✓Open banking connection in under 60 seconds

- ✓Immediate value: see your subscriptions, fees, BNPL

- ✓Viral mechanics: share savings with friends

🚀 Expand

- ✓Convert engaged users to Pay by Bank revenue stream

- ✓Merchant re-engagement: toggled-off subs trigger offers

- ✓Wallet: single product combining insights + payments

- ✓Revenue from merchant-side transaction fees

Wendi was not just a standalone consumer app — it was a strategic acquisition layer that supported future payments adoption.